A Tale of Two Data Bombs......And the Rand Dodged Both

- Dynamic Outcomes

- Feb 17

- 9 min read

NFP beat big at 130K. CPI came in soft. The Rand? It had its own ideas...

It was a week of heavyweight data...

...and the Rand took it all in its stride.

On Wednesday, the delayed US jobs report finally landed — 130,000 new positions versus just 70,000 expected. A huge beat. But buried in the same release? The annual benchmark revisions wiped 911,000 jobs from the 2025 record books. Markets didn't know whether to cheer or panic.

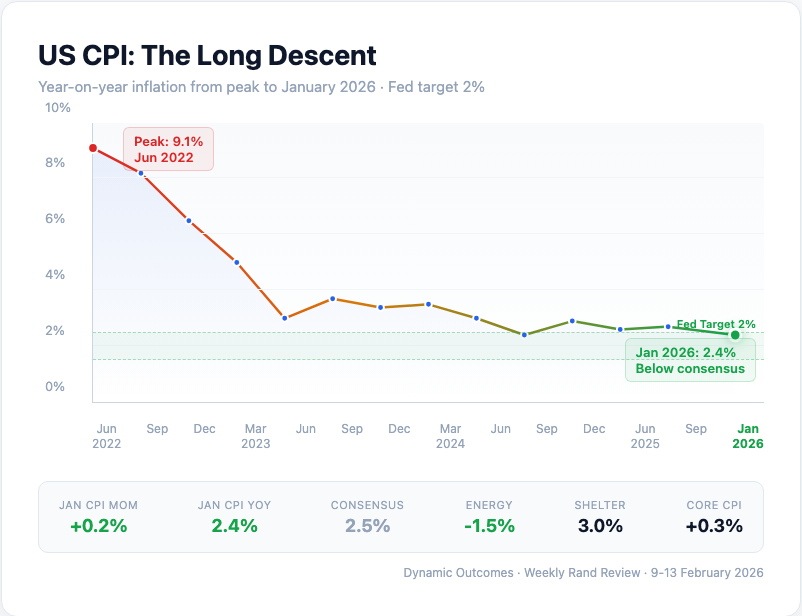

Then on Friday, CPI came in cooler than expected — 2.4% year-on-year, below the 2.5% consensus. Energy costs dropped 1.5%. Rate cut hopes flickered back to life.

Through it all, the Rand quietly went about its business...

...strengthening for a third consecutive week to close at R15.94/$ — a 10-cent gain (0.6%).

Here's how it all played out...

Key Moments (9-13 Feb 2026)

These were some of the major headlines and events over the past five days:

• Mining Indaba Opens in Cape Town: Africa's premier mining conference draws 10,000+ delegates — partnerships and investment in focus

• NFP Beats Big at 130K: Delayed January jobs report smashes 70K consensus — but 911,000 jobs erased from 2025 benchmarks

• US CPI Cools to 2.4%: January inflation lighter than expected — energy costs drop 1.5%, shelter eases to 3%

• China Grants Zero Wine Tariffs: CAEPA deal deepens — South African wine gets duty-free access to Chinese market

• SA Mining Output Rises 2.5%: December production beats expectations — iron ore and manganese lead the way

• AI Fears Tank Markets: S&P 500 drops 1.5% Thursday on tech capex concerns — Dow loses 669 points

_____________________________________________________________________

Monday: Strong Start Sets the Tone

Monday opened at R16.04/$ and the Rand wasted no time pressing stronger...

...with early trade pushing through R16.00 and accelerating.

By mid-morning, we'd broken below R15.95 and kept going. The Mining Indaba had opened in Cape Town — Africa's biggest mining conference — and the mood was optimistic. Gold was holding above $5,000 (and would push through $5,070 by midweek), the Dow was flirting with fresh records, and EM currencies were catching a bid.

The Rand powered through the afternoon, touching R15.87 before a slight pullback into the close.

Closed at R15.90/$ — a 14-cent gain and the strongest single-day move of the week.

Tuesday: Consolidation Day

Tuesday opened at R15.90/$ and the pace slowed considerably as markets settled into a holding pattern ahead of Wednesday's NFP.

Early trade saw a slight drift weaker, testing R15.95 mid-morning. With the delayed January jobs report looming, traders weren't willing to push positions too aggressively in either direction. (Can you blame them? After last week's 126-cent chaos, a quiet day was almost welcome.)

The Mining Indaba continued in Cape Town, but no major market-moving headlines emerged.

Closed at R15.94/$ — a 5-cent weakening, but essentially flat. The market was holding its breath.

Wednesday: NFP Delivers a Double Shock

Wednesday opened at R15.95/$ and all eyes were on the delayed jobs report...

...which landed with a bang.

The January Non-Farm Payrolls came in at 130,000 new jobs — nearly double the 70,000 consensus. That's a massive beat by any measure. And remember, this report had been delayed almost a week by the partial government shutdown. Markets had been flying blind since late January.

But here's where it gets interesting...

...buried in the same release were the annual benchmark revisions.

And they were brutal. The BLS revised away 911,000 jobs from the 2025 totals. December was also revised down from 50,000 to 48,000. The immediate narrative? That last year's labour market was significantly weaker than the headline numbers had suggested. (Though as we'll see below, there's a more interesting read on this.)

So what do you do with 130K new jobs when 911K old ones just vanished? Markets weren't sure either. The dollar initially firmed on the beat, pushing USDZAR briefly towards R15.96...

...but the benchmark revisions took the wind out of the greenback's sails.

By close of play, the Rand had actually strengthened — finishing at R15.86/$ — a 9-cent gain. The market decided the revisions were the bigger story.

And in other news...

Mining Indaba: Africa Digs In

Cape Town played host to over 10,000 delegates this week as the 32nd Mining Indaba got underway...

...and the theme was "Stronger together: Progress through partnerships."

The timing couldn't have been more relevant. With SA's mining sector showing signs of life (more on that below), and the global scramble for critical minerals accelerating, Africa's mineral wealth is suddenly a hot topic again.

The conference ran from Monday through Thursday, bringing together mining leaders, investors, and government officials from across the continent. No major deal announcements moved the Rand directly — but the sentiment was constructive. Africa's $29.5 trillion in mineral resources is increasingly being viewed as a strategic asset in the new geopolitical order.

The China Wine Deal — And the Bigger Picture

Remember last week's CAEPA framework signing?

...it's already bearing fruit. (Or should I say, grapes.)

On Wednesday, details emerged that China will grant zero tariffs on South African wine exports under the new trade pact. For SA's wine industry — which has been battered by the 30% US tariffs — that sounds like a lifeline.

But before we celebrate the "pivot East"...

...let's zoom out and look at what's actually happening globally.

Since Trump launched his reciprocal tariff strategy last April, over 50 countries have come to the negotiating table — and over 20 have signed actual deals or framework agreements, including the EU, UK, Japan, South Korea, and India. Many of them have agreed to zero or near-zero tariffs on US goods. Cambodia eliminated tariffs on 100% of US industrial and agricultural goods. The EU agreed to zero duties on American industrial imports. Switzerland, Malaysia, Indonesia — the list keeps growing.

This is the part that doesn't get enough airtime. Trump has been saying since 1987 — when he took out full-page newspaper ads declaring "Let's not let our great country be laughed at anymore" — that the US was getting ripped off in trade. Almost 40 years later, his strategy is doing exactly what he said it would: forcing trading partners to the negotiating table and levelling the playing field.

So when China offers SA zero wine tariffs, that's not necessarily generosity...

...it's geopolitical positioning. China is trying to pull SA closer at precisely the moment when global trade relationships are being rewritten. SA isn't just finding a new market — it's being courted as a piece on a much larger chessboard.

And as we said last week — the real question isn't whether the deal gets signed. It's: for whose ultimate benefit?

When has a deal with Beijing ever put ordinary citizens first? Will zero wine tariffs genuinely create jobs and wealth for SA wine farmers and their workers? Or will the benefits flow primarily to well-connected cronies on both sides, while ordinary Saffers see little of the upside? History suggests healthy skepticism is warranted.

The full CAEPA deal is expected to be formalised by end of March. How SA navigates between Washington's tariff pressure and Beijing's zero-tariff courtship — and who actually benefits — will be one of the defining themes of 2026.

DOGE: One Year On — And the Economy Kept Going

A quieter headline this week, but one worth noting...

...it's been a year since the DOGE-driven federal workforce reduction began.

The scale is significant. Over 322,000 federal workers have exited the workforce — the largest peacetime reduction on record. The government now employs 2.08 million people, about 10% less than in 2024. USAID was cut by 92%. HHS shed 20,000 positions.

But here's the thing the legacy media coverage consistently misses...

...the private sector kept creating jobs anyway.

Think about it. Strip out 322,000 government positions. Revise away 911,000 from the 2025 benchmarks. And STILL, the January print comes in at 130,000 new jobs — nearly double consensus. That's not a sign of a weak labour market. That's a sign of an economy that's healthier than the government-padded numbers ever suggested.

The benchmark revisions didn't reveal hidden weakness. They revealed how much of the "strength" was artificial — government headcount being counted as economic activity. Remove that padding, and what's left? A private sector that's still expanding, still hiring, and still beating expectations.

For the Rand, this matters. A genuinely resilient US economy (not just a government-jobs mirage) means the dollar's fundamentals are actually on firmer ground than the headline revision suggested.

To get back to the Rand...

Thursday: CPI Eve Jitters

Thursday opened at R15.87/$ and the Rand felt the pullback...

...as global markets took a hit.

The S&P 500 dropped 1.5% during the US session — falling from near-record territory — as AI-related stocks got hammered. Rising skepticism about the scale and returns of AI capital expenditure sent shockwaves through the tech sector. The Dow lost 669 points — its worst day in weeks. Bitcoin, still licking its wounds from last week's crash, slipped below $67,000 as risk appetite evaporated.

Back home, Stats SA released December mining production figures — up 2.5% year-on-year, beating expectations. Iron ore (+19%) and manganese (+40.4%) led the way, offsetting weakness in PGMs and coal. For the full year 2025, mining output was up just 0.1% — flat, but at least not shrinking.

The Rand gave back ground through the session, testing R15.99 before settling.

Closed at R15.96/$ — a 10-cent weakening. But context matters: this was a global risk-off move, not a Rand-specific story.

Friday: CPI Soothes the Market

Friday opened at R15.95/$ and the early session was cautious...

...with traders positioned ahead of the US CPI release.

The numbers landed mid-morning US time. January CPI came in at +0.2% month-on-month, below the 0.3% consensus. Year-on-year, headline inflation eased to 2.4% — cooler than the 2.5% expected. Core CPI (excluding food and energy) was in line at 0.3%.

The detail? Energy costs fell 1.5% — the biggest drag on headline inflation. Shelter costs, which make up a third of CPI, rose just 0.2% — bringing the annual rate down to 3%. Used car prices dropped 1.8%.

Markets liked it. The S&P 500 bounced 0.7% and the Dow added 251 points, recovering some of Thursday's losses. The dollar softened, which should have helped the Rand...

...but the pair spiked to R16.08 briefly before pulling back. At the time of writing, we're trading around R15.94 — essentially flat on the day.

Why the spike? Probably technical — Friday profit-taking after a strong week, plus some position adjustment ahead of the weekend. The DHS funding continuing resolution also expires today (13 February), adding a layer of uncertainty about another potential government shutdown.

Volatility & Risk Analysis

Here's how the volatility played out:

• Open to Close Move: The week opened at R16.04/$ Monday morning and closed Friday afternoon at R15.94/$ — a 10c strengthening (0.6%) for the week.

• Average Daily Range: ~15c (0.9%) — Risk per $1 Million Exposure: R150,000

• Maximum Single-Day Move: ~21c (1.3%) on Monday — Risk per $1 Million Exposure: R210,000

• Weekly Range: 27c (R15.81 low to R16.08 high) — 1.7% swing — Risk per $1 Million Exposure: R270,000

• Maximum Intraweek Strength: -23c (-1.4%) from Monday open to Thursday low (R15.81)

• Maximum Intraweek Weakness: +15c (+0.9%) from Thursday low to Friday high (R16.08) — a sharp intraday reversal

For exporters with USD receivables, Friday's spike to R16.08 was actually the week's best conversion opportunity — briefly surpassing even Monday's opening at R16.04. If you caught that window, you locked in the weakest Rand level of the week. For importers needing to buy USD, Thursday's dip to R15.81 was the gift — the cheapest dollars since late January.

The 27-cent range is exactly half of last week's 53-cent swing. Volatility compressed sharply, which makes sense: after the tariff chaos, China deal, and crypto crash of the previous week, markets needed to digest. This week was that digestion — steady, methodical, and ultimately constructive for the Rand.

The Week Ahead (17-21 February 2026)

SA: Retail Sales (Tuesday), SARB MPC Preview commentary, Budget Speech preparations (26 Feb)

US: Retail Sales (Tuesday), FOMC Minutes (Wednesday), Initial Jobless Claims (Thursday), Leading Indicators (Friday)

EU/Global: UK CPI (Wednesday), ECB commentary

What to Watch

The FOMC Minutes on Wednesday will be closely watched for any signals about the March meeting. The January CPI print was soft enough to keep rate cut hopes alive — but the strong NFP complicates the picture. Markets want to know: does the Fed see the benchmark revisions as a reason to cut sooner?

Back home, all eyes are starting to turn to the Budget Speech on 26 February. Finance Minister Enoch Godongwana will need to balance fiscal consolidation with growth support — and markets will be watching for any signals on debt trajectory, revenue performance, and the GNU's spending priorities.

The Rand's three-week winning streak faces its first real test: can the momentum hold through a quieter data week, or will profit-taking kick in?

Until next week — stay sharp, stay skeptical, and don't let the headlines do your thinking for you.

To your success~

_____________________________________________________________________

This weekly newsletter is brought to you courtesy of Dynamic Outcomes, a Rand forecasting service focused on assisting exporters, importers and individuals in making more informed and educated decision around the timing of their foreign currency transaction – a critical factor in any risk management strategy. This is centred around providing an objective view of where the Rand is expected to move against the Dollar, Euro and Pound over the short, medium and long term.

BeztForex have arranged for our clients to try out the Dynamic Outcomes Rand forecasting service for a full 14 days at no cost and no obligations:

________________________________________________________________________

Disclaimer: The content of this Weekly Rand Review has been prepared by and constitutes the opinion of Dynamic Outcomes, a division of Dynamic Forex Solutions LLC (DFS); it is solely for informational and educational purposes and is not to be taken as advice, or an offer or solicitation to buy or sell the securities or financial products mentioned in the content nor a recommendation to participate in any particular trading strategy. No past performances of any strategy or forecasts are a guarantee of future performance; trading in financial markets involves substantial risk, and you need to do your own due diligence in managing this risk. While every care has been taken in ensuring that the content gleaned from third parties is from reliable sources, no responsibility or liability will be accepted by BeztForex or DFS as to the accuracy of the information contained here, which may be subject to correction or amendment at any time after publication.

Comments